China hardware-first vs US AI-first: the robotics divide of 2026

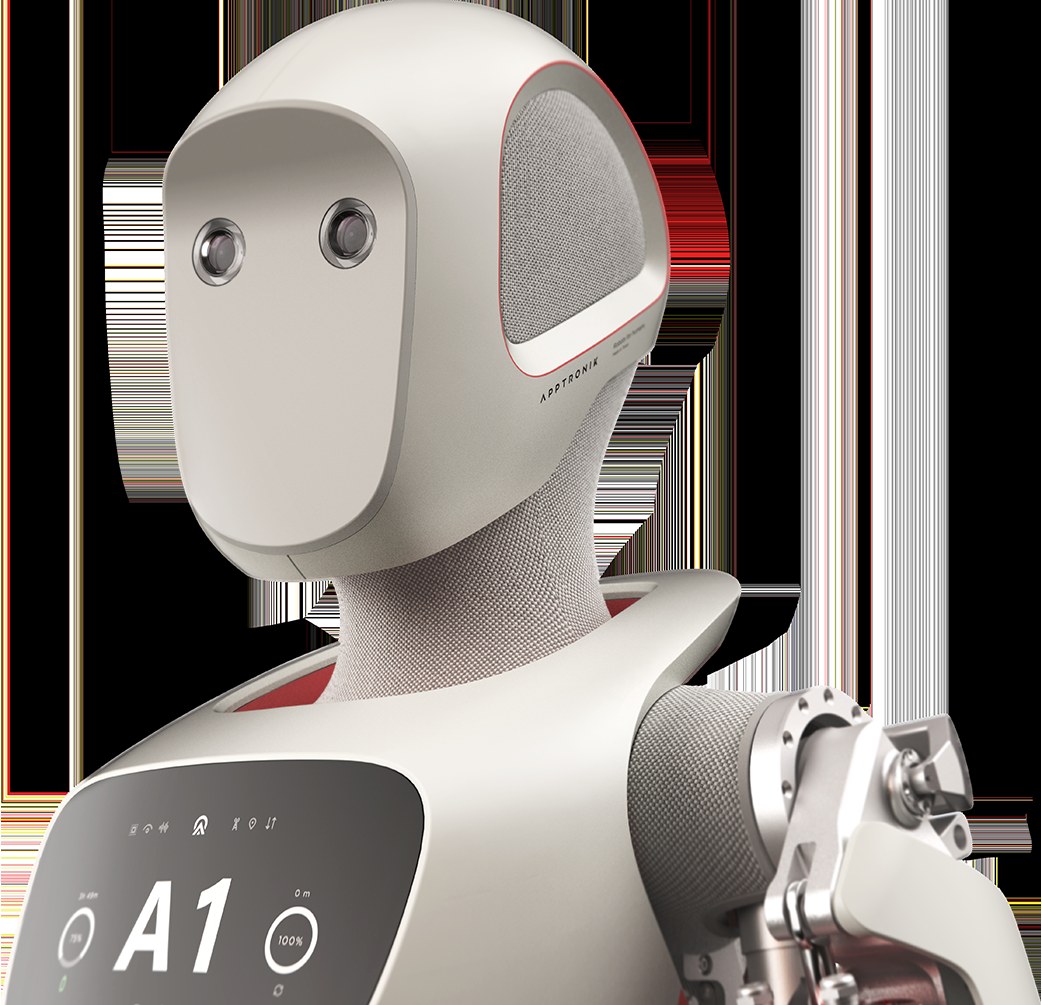

US robotics is AI-first. Boston Dynamics, Figure, 1X, Apptronik, Tesla — each is racing on model quality. The foundation models, the imitation learning stacks, the language-grounded action selection —

US robotics is AI-first. Boston Dynamics, Figure, 1X, Apptronik, Tesla — each is racing on model quality. The foundation models, the imitation learning stacks, the language-grounded action selection — these are where US companies invest, raise, and recruit.

China robotics is hardware-first. Unitree, Galbot, AgiBot, XPeng, Astribot, Booster, UBTECH, LimX, DEEP — each is racing on chassis cost, manufacturing density, and time-to-market. Build the body cheap and shipping; fix the brain in the field.

The GD01 is hardware-first incarnate. A 500kg transformable mecha with a human pilot inside. No AI dependency. No foundation model bottleneck. The operator is the autonomy. Unitree could ship this in volume the day they wanted to. It is the most extreme expression of the divergence.

Implications. (1) Procurement: a buyer wanting a working robot today gets a Chinese hardware-first solution; a buyer betting on autonomy timelines gets a US AI-first system. (2) Geopolitics: the export-control regime targets foundation models and high-end compute, which favors the US AI-first stack. It does not target piloted mechs. (3) Total addressable market: the AI-first roadmap unlocks $1T+ services markets if it works; the hardware-first roadmap unlocks $50-100B equipment markets that already exist. Different bets, different timelines.

The winning thesis is probably both. Hardware-first wins the next 24 months on shipments. AI-first wins the decade if autonomy delivers. The interesting question is whether US AI-first players can win without a hardware platform of their own — and whether Chinese hardware-first players can graft autonomy onto a chassis that was not designed around it.